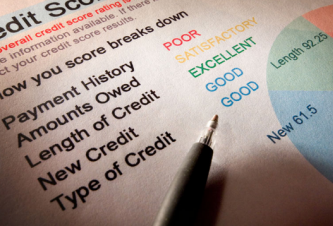

Credit Literacy Quiz

The reality today is we are facing the toughest financial era since the Great Depressio n. Despite the massive amounts of resources being assembled in the cause of financial education, year after year, surveys uncover that people all over the country are as financially and credit illiterate as ever.

n. Despite the massive amounts of resources being assembled in the cause of financial education, year after year, surveys uncover that people all over the country are as financially and credit illiterate as ever.

In order to win this battle requires us to be diligent and continue to utilize all the invaluable resources available to us.

My passion lies in educating consumers and business owners with the credit knowledge and resources they need to utilize the power of credit to their advantage.

Click to continue …

I was excited to write this particular post because there is such a tremendous lack of awareness in the entrepreneur and small business community surrounding the business credit industry.

I was excited to write this particular post because there is such a tremendous lack of awareness in the entrepreneur and small business community surrounding the business credit industry. Marco Carbajo is a business credit expert, author, speaker, and founder of the Business Credit Insiders Circle. He is a business credit blogger for Dun and Bradstreet Credibility Corp, the SBA.gov Community, About.com and All Business.com. His articles and blog; Business Credit Blogger.com, have been featured in ‘Fox Small Business’,’American Express Small Business’, ‘Business Week’, ‘The Washington Post’, ‘The New York Times’, ‘The San Francisco Tribune’,‘Alltop’, and ‘Entrepreneur Connect’.

Marco Carbajo is a business credit expert, author, speaker, and founder of the Business Credit Insiders Circle. He is a business credit blogger for Dun and Bradstreet Credibility Corp, the SBA.gov Community, About.com and All Business.com. His articles and blog; Business Credit Blogger.com, have been featured in ‘Fox Small Business’,’American Express Small Business’, ‘Business Week’, ‘The Washington Post’, ‘The New York Times’, ‘The San Francisco Tribune’,‘Alltop’, and ‘Entrepreneur Connect’.

Recently I shared the benefits of building business credit with each of the business credit agencies. Separation of personal and business credit is a must for small business owners in order to eliminate personal liability and protect the integrity of the corporate veil.

Recently I shared the benefits of building business credit with each of the business credit agencies. Separation of personal and business credit is a must for small business owners in order to eliminate personal liability and protect the integrity of the corporate veil.